REIT Dividends

Real estate investment trusts are known for their dividends, due in part to the inflationary nature of rents and property values… and even more so to the REIT structure itself. By law, these entities must pay out at least 90% of their taxable income to shareholders in the form of dividends.

As a result, REIT dividends – as a percentage of their free cash flows – tend to be higher than those of other companies. And REIT shares normally trade at higher dividend yields.

According to Ed Clissold, an equity strategist at Ned Davis Research (as referenced in a September 2010 Barron’s article), the S&P 500 index delivered average annual price appreciation of 4.92% from the end of 1929 until 2009, but its average annual total return was 9.16%.

Therefore, dividends provided approximately 46% of those total returns.

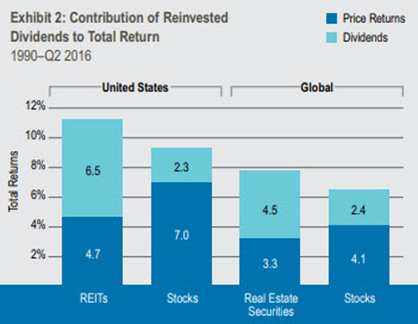

REIT dividends, meanwhile, can be even more effective. As illustrated below, they have comprised more than half of the returns for U.S. and global REITs – significantly more than those of the broad equity markets.

While REITs haven’t been on the market as long as many other investing options, they still have a well-established history of consistently raising dividends. From the early 1990s through 2007, U.S. REITs increased their payouts at an average annual rate of 5.8%.

With the onset of the global financial crisis in 2008, it’s true that many REITs cut their dividend payouts to the minimum required level in order to preserve capital. (More about this further down below.) They also began issuing portions of those dividends in common stock.

However, as conditions – and cash flow – have improved across nearly all property sectors, cash dividends have made a strong comeback. And U.S. REITs should continue to see healthy dividend growth over the next several years.

Cash flow growth can come organically from rising rents and occupancies, or externally from development and acquisitions. Regardless, as a REIT’s income increases, it must ensure that its distribution rate remains above the level required by law, which often means it must raise its dividend.

There’s no other choice on the company’s part which suits investors just fine.

As of fourth quarter 2018, dividends paid by equity and mortgage REITs totaled $13.9 billion, a 1.6% decrease from the prior quarter and marginally above fourth quarter 2017 thanks to a merger transaction that prompted a shift forward of dividend payments that would normally have taken place in Q4 into Q3.

Had that not occurred, total dividend payments for the end of 2018 would have been approximately 1.9% higher and 2.1% above what they were one year earlier.

As Ralph Block explains in Investing in REITs:

There’s an intangible psychological benefit in seeing significant dividends roll in each month or each quarter. If, like most of us, you have to earn a salary, seeing a check come in for several hundred dollars – without you having to show up at the office – provides substantial comfort regardless of whether you intend to spend it or reinvest it.

And that right there is worth a lot.

Not All Dividends Are the Same

One key metric that REIT investors should always consider is the payout ratio of dividends to adjusted funds from operations, or AFFO. As these businesses issue new equity, the best managed ones make sure to retain a substantial piece of their operating income for acquisitions, developments, and other opportunities.

This is smart, long-term thinking since, in the end, using retained capital for such activities is cheaper than raising debt capital or selling new shares.

That’s why a modest payout ratio is actually a good thing. It acts as insurance against unexpected events that might cause temporary downturns in free cash flow.

No matter how traditionally safe REITs can be, it’s important to remember that they operate in cyclical industries that do fall on distressed credit markets and similarly unwanted economic movements when they come around. Real estate investors also need to prepare for unforeseen lawsuits, tenant bankruptcies, and other negatively impactful possibilities.

As referenced above, most REITs were forced to cut their dividends in 2008 and 2009, leaving only a handful that were able to increase their payouts during that period.

Those stalwart REITs should be commended, and perhaps invested in as well. They planned. They prepared. And they came out ahead as a result.

CHART HERE

Watch Out for Sucker Yields

While the financial crisis of 2008 came as a major surprise to most, there were warning signs. There usually are.

The same thing goes for individual investment entities operating under individual circumstances. When a REIT pays out too much of its AFFO in dividends, it opens up more risk of having to cut its dividend in the future, with its stock price taking a likely hit as well.

Here at iREIT, we call this recipe for disaster a sucker yield.

When a company is paying a dividend beyond its earning power, it’s essentially eroding capital. Suppose a company is paying a 10% or higher yield. In that case, there’s a good chance that it already has a track record of cutting its payouts. Its balance sheet will probably feature considerable leverage as well.

When a stock is paying an extraordinarily high dividend yield combined with an unsustainable business model, there will almost always be loss of principal.

As referenced on the REIT Valuation page, AFFO is superior to its calculating cousin (funds from operations, or FFO) in determining a REIT’s free cash flow. If a REIT claims to have earned $1.20 per share in FFO but uses $0.20 for recurring capital expenses, that leaves it with no more than $1.00 for dividend payments.

And if it does, in fact, pay out that whole $1.00, then it has nothing left – no margin of safety – to expand the business or set aside funds for unforeseen expenses.

As we’ve already established, that’s a problem. A major one.

Even so, we know the lure of a sucker yield is strong. But fight it anyway. The innate desire to chase those higher numbers leads to the same thing that all such single-minded chasing does… impulsively obtaining dividend quantity over dividend quality.

Companies that fall under the “sucker yield” definition tend to have unpredictable and unreliable earnings histories with unsafe dividend payouts.

You don’t want a part of them.

The Monthly Paying REIT

As referenced on the REITs Around the Globe page, most Canadian real estate investment trusts pay out monthly dividends, as opposed to quarterly. Apparently, that’s because most REIT investors in Canada are retail investors. The institutional ones prefer to invest directly in private real estate.

Alternatively, while there are a few publicly traded REITs in the U.S. that operate on that same monthly basis, most of them work with quarterly dividends. (Note: most non-traded REITs, however, do pay monthly).

Going forward, we would like to see more of them convert to monthly models. This switch would require very little effort on their part while offering investors automatic and obvious benefits.

What About the Tax Man?

Just because a REIT pays out at least 90% of taxable income in the form of dividends doesn’t mean that Uncle Sam misses out on his bite of the apple. He always gets his bite of the apple, make no mistake.

In this case, it’s mainly by way of investors.

For REITs, dividend distributions are considered to be either ordinary income, capital gains, or return of capital… each of which may be taxed at a different rate. Keep in mind that many REITs pay dividends to shareholders in excess of net income (as defined by the IRS), and a significant part of that excess is often treated as “return of capital” to the shareholder.

This makes them non-taxable as ordinary income.

All public companies, including REITs, are required early in the year to provide shareholders with information that clarifies how the prior year’s dividends should be allocated for tax purposes. A Historical Record of the allocation of REIT distributions between ordinary income, return of capital, and capital gains can be found in the Industry Data section.

The 2017 Tax Cuts and Jobs Act

The 2017 Tax Cuts and Jobs Act introduced several new measures that do affect REITs, including a 20% deduction on pass-through income. This deduction applies to businesses that operate as pass-through entities, REITs included.

Since REIT dividends are taxed at the individual shareholder’s rate rather than the corporate rate, the 20% pass-through deduction reduces their top tax rate from 39.6% down to 29.6%. And shareholders in the lower brackets have an even lower rate on the same dividends.

This change could prove to be significant for REIT investors, more so than the across-the-board reductions in individual tax rates.

Ordinary income historically represents about 60% of REIT distributions, with the rest generally categorized as a mix of capital gains (which are taxed at no more than 20%) and return of capital (which are tax-deferred until shares are sold). The Medicare surcharge for higher earners on net investment income remains at 3.8%.

The new deduction improves on an already tax-efficient vehicle. Since REITs are pass-through entities, the income is taxed only once at the shareholder level. In addition, because they generally don’t pay corporate taxes, they have more income to distribute. This is a large part of why REITs have historically paid higher dividends than the S&P 500 average, as referenced on the REIT Dividends page.

Section 199A of the tax code further details the rules for qualified business income, or QBI, showing how REIT investment returns are eligible for a 20% deduction. You’ll find the appropriate amounts on Line 5 of Form 1099-DIV.

Use the Form 1040 instructions, particularly on page 2, line 9, to figure out any tax deduction on your recorded amount.

THIS CHART shows the U.S. withholding tax rate on REIT ordinary dividends paid to non-U.S. investors.

Bottom line: Always remember that tax efficiency (i.e., making sure you don’t pay more taxes than you have to) is a cornerstone to any well-balanced portfolio. Knowing this, you might want to consider consulting a tax professional for advice.